Get your priorities right from the start.

Let’s face the reality that the present situation has forced many businesses to a complete stop. However, with or without support from its governments, businesses will eventually reopen and start operating. Most of business owners will aim to get back fast to where they were before the Covid-19. The revamp of the business might be even fast at the beginning but that is when the problems may start to appear.

Ask yourself a question: How much experience do you have in starting a business or do you really remember how it was in the early times of your business? The Post-Covid-19 reboot may be similar to starting a business from scratch. In that case, specific approach needs to be made to get your business up and running again. There are many areas that will need attention, such as: employees, sales and marketing, products, suppliers, facilities, health and safety regulations, etc. and it will need capital, very much the same when starting a business.

So, one thing is how to fund your Post-Covid-19 business and the second is how to effectively manage your cash flows. Under normal circumstances, company management pays more attention to profits, but during market crashes, cash becomes a commodity that cannot be overlooked. In turbulent times, even large and global companies need to focus on their liquidity. Same thing applies to small and medium companies.

Does management understand the cash flow?

The cash flow reporting as a term may be known to company management but they may lack understanding how to apply it in everyday business. Particularly, when their performance has been measured only on profit and loss results and no or little attention was made to the structure of the company’s balance sheet or use of financial resources as presented in a cash flow statement. If the company management does not feel comfortable with cash flow concept they will be reluctant to reprioritize their actions and help company overcome liquidity issues. That may eventually lead to a bankruptcy.

Good examples are two big names: General Motors, which filed for a government-backed Chapter 11 reorganization on June 8, 2009 and Chrysler Corporation, which did the same thing a bit earlier on April 30, 2009. Meanwhile the third USA automotive company, Ford Motor Company, has survived the industry crisis of 2008–2010 because its management was strongly committed to avoid Chapter 11 bankruptcy. Ford top management was aware of solvency risks during the coming downturn and devoted resources in advance to manage their liquidity. They have even provided cash flow management trainings to its staffs in operations to emphasize the significance of proper use of funds.

What is the cash flow statement and forecast?

The cash flow statement shows how in the past cash has been received and used by the company in an aggregated format. It is a financial statement along with a profit and loss account and balance sheet, and it is a bridge between them. The purpose of the cash flow statement is to provide stakeholders with information about the company's financial condition in terms of the possibility of continuing operations and generating cash for investors.

The cash flow statement consists of three sections and each of them is very important: Operational, Investment and Financial activities. Operating cash flow is the most important section from a business point of view as it measures how much cash is generated by the core business. Investment activities show, among other things, important aspects of whether a company is investing money back into its business in order to survive or grow in the long term. Finally, the third section, Financing activities, tells a lot about how the business is funding its operations and manages company’s equity as well as external debt. This last part of cash flow is important for investors to understand what return on investment they can expect in the future.

These three sections of the cash flow statement add up to Net Cash for the period. Net Cash is reconciled with changes in the company's bank accounts, so it represents a tangible value that has been physically proven. There are no accounting adjustments. If Net Cash differs radically from Net Profits reported by the company, it is worth knowing the reasons for this situation. This does not mean that it is wrong, but rather indicates that important actions have been taken within the company that are not reflected in the income statement.

Net cash will not tell us directly how well a business is doing as it includes all cash flow such as investments in financial assets, newly raised capital, paid dividends, or changes in debt. Therefore, positive Net Cash does not necessarily tell us that the business is properly managed. Quite often, another number, called Free Cash Flow, is calculated instead.

The Free Cash Flow is derived from Operating cash flows less capital expenditures. Capital expenditure, known as CapEx, is expenditure on property, plant and equipment. CapEx is needed to keep the company's assets in good working conditions. Therefore, Free Cash Flow is a measure of how well a company generates cash from its operations and maintains its business over the long term. If Free Cash Flow has been negative for several years and not supported by investment in growth, the firm is likely poorly managed. Free Cash Flow is often used to make better investment decisions and is part of the cash flow forecast.

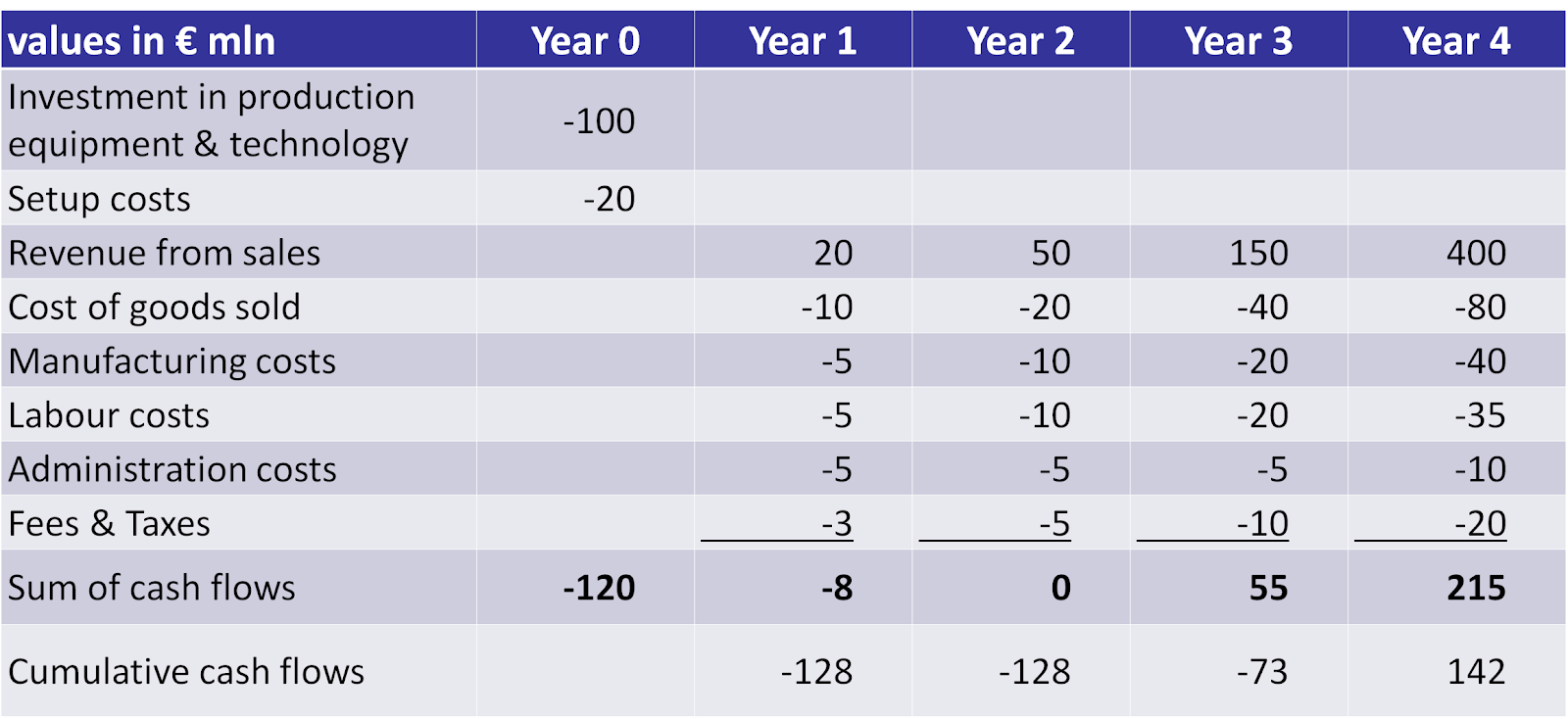

A cash flow forecast differs from a cash flow statement in that it is a projection for the future and the cash flow statement is based on historical performance. A cash flow forecast is a plan of future cash inflows and outflows over a specified period of time, such as several months, quarters, or years. Its purpose is to tell management how much cash the company will use or generate during this period. The plan also shows how much outside cash the company will need to continue its operations and achieve strategic goals.

A cash flow forecast can follow a similar three-section layout to a cash flow statement to facilitate comparison between forecasts and past performance. However, for smaller organizations, it makes sense to focus primarily on forecasting Operational cash flows and investments (CapEx). This will show changes to Free Cash Flow instead of Net Cash. Such a forecast will help assess the business potential and identify any problems. Net Cash calculation can be added after operating plans are established.

A typical cash flow forecast will have the characteristics shown in the "Cash movements" chart below.